KiwiSaver is a voluntary savings scheme to help employees set up for their retirement. Contributions are divided into two portions:

Employee contributions - these are deducted from the employee’s pay

Employer contributions - these are paid by the employer on top of the employee’s pay, and are subject to Employer Superannuation Contribution Tax (ESCT)

Learn about KiwiSaver

As an employer, you should familiarise yourself with your KiwiSaver responsibilities. For all the details, visit ird.govt.nz/kiwisaver.

Setting up an employee's KiwiSaver

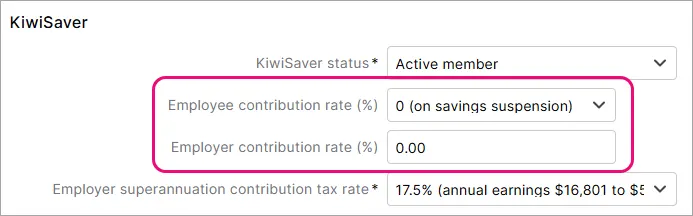

When adding an employee into MYOB, you'll set up their KiwiSaver status and contribution rates (Payroll menu > Employees > click the employee > Employment tab).

Here are some more details about each of the KiwiSaver fields shown above.

KiwiSaver status | Active member – the employee is currently enrolled in KiwiSaver Auto enrol new employee – the employee meets the automatic enrolment criteria (learn more on the IR website) Opting in existing employee – the employee is choosing to opt into KiwiSaver (learn more on the IR website) Not eligible – the employee is not eligible to be in KiwiSaver (check eligibility criteria on the IR website) Casual or temporary employee – when you have a new employee who is not subject to automatic enrolment due to being a casual or temporary employee (learn more on the IR website) Opted out – the employee was auto-enrolled but they want to leave the KiwiSaver scheme (learn more on the IR website) |

Employee contribution rate (%) | For all active KiwiSaver members, a percentage of pay must be deducted for KiwiSaver contributions. The minimum legal contribution is 3.5% of an employee’s pay, but they may choose to contribute either 4%, 6%, 8% or 10% instead. Your employee will inform you if they want to change their contribution rate. You can also set this to 0 to suspend contributions - see below for details. |

Employer contribution rate (%) | If your employee is an active KiwiSaver member, you are required to make employer KiwiSaver contributions of at least 3.5% of the employee’s pay. These contributions are subject to Employer Superannuation Contribution Tax (ESCT). ESCT is reported to Inland Revenue as part of payday filing. |

Employer superannuation contribution tax rate | All employer contributions are subject to ESCT. The amount of ESCT to be paid on your employer KiwiSaver contributions is based on the employee’s expected annual salary. Any ESCT amounts will be automatically included when you process the employee’s pay, based on your selections on the KiwiSaver tab for each employee. To learn more about ESCT and for help working out an employee's rate, visit ird.govt.nz |

Suspending KiwiSaver contributions (contribution holidays)

Employees can apply to Inland Revenue (IR) for a contribution holiday. You (their employer) will be notified if a contribution holiday is granted, either by IR or by the employee. For more about employees applying for a savings suspension, see this IR information.

During a contribution holiday, you need to stop deducting KiwiSaver contributions from the employee’s pay, and you are not required to make any employer contributions.

You will be notified when the contributions holiday ends and you need to resume contributions.

If an employee is on a contributions holiday, you're not required to make any employer contributions, but you may still choose to do so.

To suspend KiwiSaver contributions

Go to the Payroll menu > Employees.

Click the employee's name.

Click the Employment tab.

Under KiwiSaver, click the dropdown arrow for Employee contribution rate (%) and choose 0 (on savings suspension). This will also change the Employer contribution rate (%) to 0.00.

Click Save.

To resume contributions, repeat these steps and choose the applicable Employee contribution rate (%).