A closely held employee is someone who's directly related to the business, company or trust that pays them, such as:

family members of a family business

directors or shareholders of a company

beneficiaries of a trust.

The ATO refers to these as closely held payees, but as we'll explain below you'll set them up in MYOB as employees—so that's how we'll refer to them.

Reporting closely held employee payments to the ATO

The ATO require payments to closely held employees to be reported via STP at least quarterly. So if you're paying a closely held employee on a regular frequency, such as weekly, fortnightly, monthly or quarterly, you can process their payments through payroll like any other employee. This will also take care of the tax and superannuation obligations which are required on those pays. Learn all about setting up an employee and processing your payroll.

However, if a closely held employee isn't paid on a set frequency, you'll still need to report their pays to the ATO via STP at least quarterly.

Here is the recommended way to handle these types of quarterly payments.

Seek expert advice

Quarterly reporting might not suit your business needs, so you should speak to your accounting advisor about what works best for you.

1. Set up a closely held employee

You'll set up a closely held employee in much the same way as any other employee (Create menu > Employee > enter the employee's name and email and deselect the option Invite employee to fill out their own details > Continue).

There's some additional mandatory information you'll need to enter in the employee's record to be able to report their payroll information via STP.

On the Contact details tab, enter details in these fields:

First name

Surname or family name

Country

Address

Suburb/town/locality

State/territory

Postcode

On the Payroll details tab > Employment details section, enter information in these fields:

Date of birth

Start date

Employment basis

On the Payroll details tab > Taxes section, enter information in these fields:

Tax file number

Tax table

Income type (set to Closely held payees)

On the Payroll details tab > Salary and wages, set the Pay cycle to Quarterly.

On the Payment details tab, set the Payment method to Cash.

If you need a refresher on setting up an employee or you've never done it before, learn all about adding employees.

Super payments

As you'll need to pay superannuation for closely held employees, make sure you've set up Pay Super.

2. Set up STP

If you haven't already, you'll need to set up STP. You'll then be able to report your closely held employees' payroll information to the ATO each quarter.

To get started, go to the Payroll menu and choose Single touch payroll reporting.

For all the details, see Setting up Single Touch Payroll reporting.

3. Process interim payments

Because you'll be reporting payroll information to the ATO once per quarter, you'll likely need to record interim payments to reflect the more regular payments you make to closely held employees.

Each business is different, so check with an accounting advisor about the best way track, record and reconcile these interim payments.

One suggestion would be:

Create a payroll clearing category to keep track of interim payments made to closely held employees.

Set the payroll clearing category as the linked category for payroll cash payments (Accounting > Manage linked categories > Payroll tab > Bank account for cash payments).

Record interim payments as spend money transaction, allocated to the payroll clearing category. You can use your online banking software to deposit the money into the employee's account as you won't be able to create an ABA bank file for these payments.

4. Process and report a quarterly pay run

When you process a pay run for your closely help employees, you'll enter their pay amounts for the quarter (including earnings and deductions), then report it to the ATO.

Your accounting advisor will likely advise the amounts you'll need to enter into the pays.

If you've processed payroll before, this'll be easy. Here's a quick rundown—for more details see Do a pay run.

Go to the Create menu and choose Pay run.

For the Pay cycle, choose Quarterly.

Choose the pay dates and click Next. All the employees you've set up with a quarterly pay cycle will be listed. Deselect any employees you don't want to include in this pay run.

Enter the pay amounts for each closely held employee:

Click the employee to open their pay.

Enter the hours and/or amounts for each applicable pay item,

Click Next and review the details of the pay.

When you're ready, click Record.

When prompted to send your payroll information to the ATO, enter your details and click Send.

When you're done, click Close.

Remember you've already paid the employee (see task 3 above) so no payment will be required when processing the pay run.

At the end of the year

Your accountant will work with you at the end of the payroll year to ensure your books are balanced. For example, you might need to allocate any remaining balance in the payroll clearing category which hasn't been processed through payroll.

Unlike a regular employee (also called an arm's length employee), a closely held employee is someone who's directly related to the business, company or trust that pays them, such as:

family members of a family business

directors or shareholders of a company

beneficiaries of a trust.

The ATO refers to these as closely held payees, but as we'll explain below you'll set them up in AccountRight as employees—so that's how we'll refer to them.

Reporting closely held employee payments to the ATO

The ATO require payments to closely held employees to be reported via STP at least quarterly. So if you're paying a closely held employee on a regular frequency, such as weekly, fortnightly, monthly or quarterly, you can process their payments through payroll like any other employee and it'll be reported to the ATO via STP. This will also take care of the tax and superannuation obligations which are required on those pays. Learn all about setting up an employee and processing your payroll.

However, if a closely held employee isn't paid on a set frequency, you'll still need to report their pays to the ATO via STP at least quarterly.

Here's the recommended way to handle these types of quarterly payments to report them to the ATO each quarter.

Seek expert advice

Our method below might not suit your business needs, so you should speak to your accounting advisor about what works best for you.

1. Set up a closely held employee

You can set the employee up much the same as any other employee (Cards File > Cards List > Employee tab > New).

There's some mandatory information you'll need to enter to be able to report their payroll information via STP, including:

First name

Surname or family name

Address (including suburb/town/locality, state/territory, and postcode)

Tax file number

Also set the following in the employee's card:

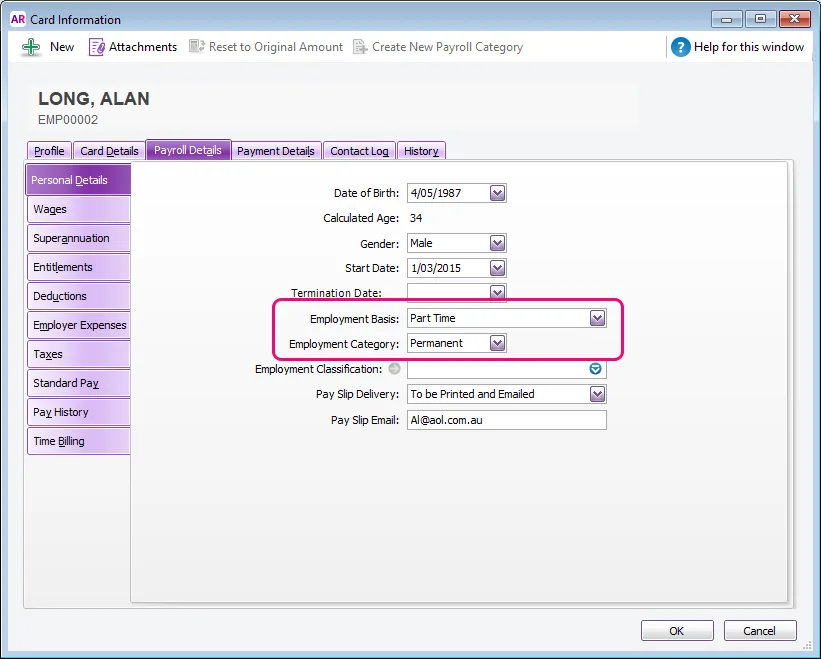

On the Payroll Details tab > Personal Details, set their Employment Basis to Full Time, Part Time or Casual (as applicable), and their Employment Category to Permanent.

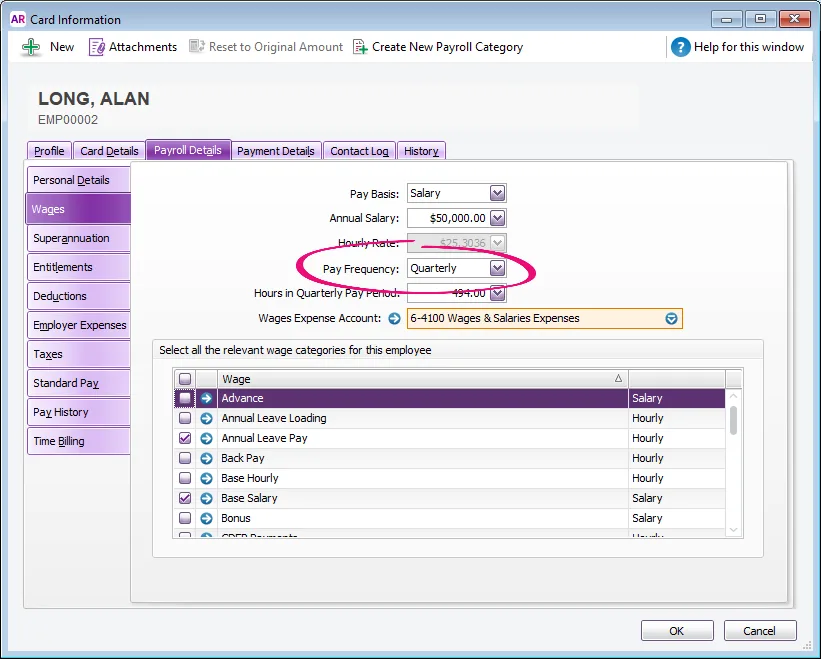

On the Payroll Details tab > Wages, set their Pay Frequency to Quarterly. Remember, this is just to allow the employee's information to be sent to the ATO each quarter and doesn't reflect how often you actually make interim payments to the employee (as covered in task 3 below).

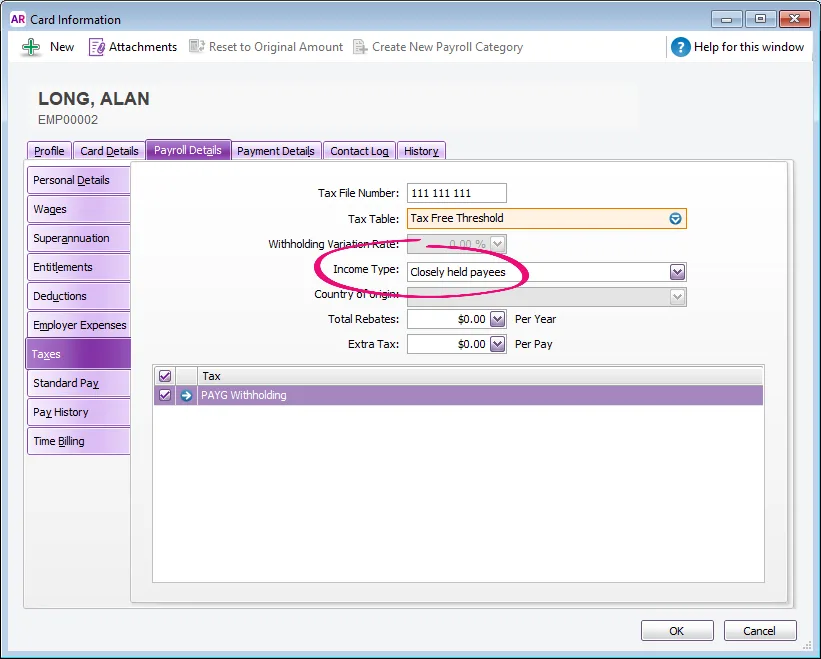

On the Payroll Details tab > Taxes, set their Income Type to Closely held payees.

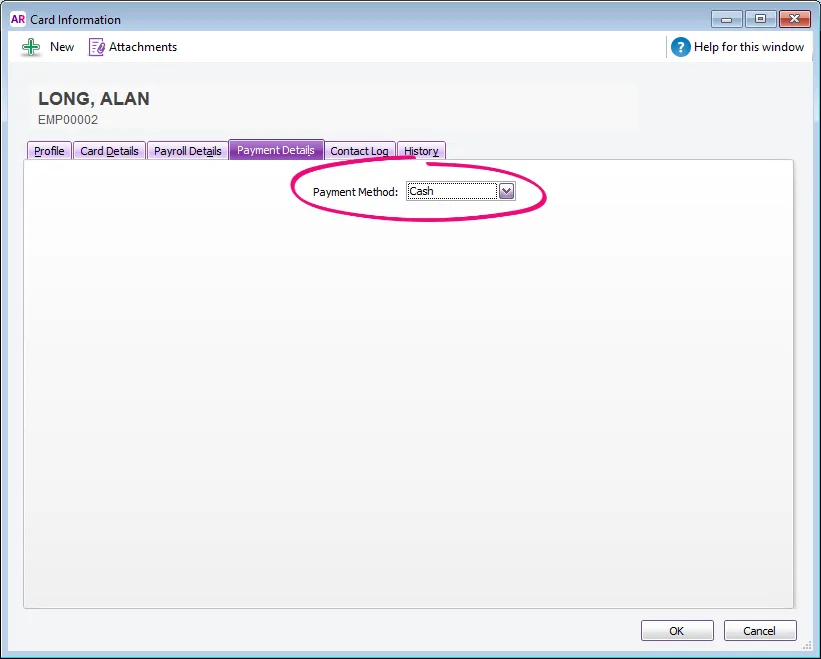

On the Payment Details tab, set their Payment Method to Cash.

If you need a refresher on setting up an employee or you've never done it before, learn all about adding employees.

Super payments

You'll need to pay superannuation for closely held employees, so make sure you've set up Pay Super and added your closely held employees to Pay Super payments.

2. Set up STP

If you haven't already, you'll need to set up STP. You'll then be able to report your closely held employees' payroll information to the ATO each quarter.

To get started, go to the Payroll menu and choose Single Touch Payroll reporting.

For all the details, see Setting up Single Touch Payroll reporting.

3. Process interim payments

Because you'll be reporting payroll information to the ATO once per quarter, you'll likely need to record interim payments to reflect the more regular payments you make to closely held employees, such as weekly or fortnightly payments.

Each business is different, so check with an accounting advisor about the best way track, record and reconcile these interim payments.

One suggestion would be:

Create a payroll clearing account to keep track of interim payments made to closely held employees.

Set the payroll clearing account as the linked account for payroll cash payments (Setup > Linked Accounts > Payroll Accounts > Bank Account for Cash Payments).

Record interim payments as spend money transactions, allocated to the payroll clearing account. You can use your online banking software to deposit the money into the employee's account as you won't be able to create an ABA bank file for these payments.

4. Process and report a quarterly pay run

You'll need to process a pay run for your closely help employees each quarter to report their payments for that quarter to the ATO. This includes all their earnings and deductions. Your accounting advisor will likely advise the amounts you'll need to enter into the pays.

If you've processed payroll before, this'll be easy. Here's a quick rundown—for more details see Processing your payroll.

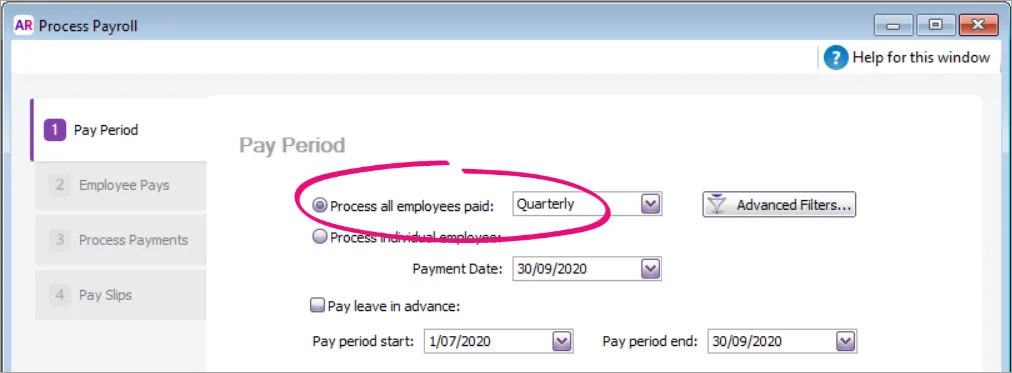

Go to the Payroll command centre and click Process Payroll.

Select the option to Process all employees paid and choose Quarterly as the frequency.

Choose the pay dates and click Next. All the employees you've set up with a quarterly pay cycle will be listed. Deselect any employees you don't want to include in this pay run.

Enter the pay amounts for each closely held employee:

Click the blue zoom arrow to open the employee's pay details.

Enter the hours and/or amounts for each applicable payroll category.

Click OK when you're done.

Click Record then click Record again at the confirmation message.

When prompted to send payroll information to the ATO, enter the name of the authorised sender and click Send.

Finish the pay run as normal. Need a refresher?

Remember you've already paid the employee (see task 3 above) so no payment will be required when processing the pay run.

At the end of the year

Your accountant will work with you at the end of the payroll year to ensure your books are balanced. For example, you might need to allocate any remaining balance in the payroll clearing account which hasn't been processed through payroll.